Union Pacific: Revenue And Safety Headwinds Present Ongoing Challenges

Summary

- Exposure to the economic cycle will weigh on Union Pacific’s top line despite pockets of growth in certain end markets.

- Lower fuel prices should aid in a lower operating ratio.

- Recent derailments by other railroads and new rail safety legislation pose profitability risk, particularly as Union Pacific embraces precision scheduled railroading (PSR) to hasten operations.

- Valuation seems relatively high compared to historical and relative standards; however, sustained value will support higher share price over long run.

About a month ago, I wrote about Parker-Hannifin (NYSE:PH), an industrial resilient to macroeconomic downturn due to its end markets and diversification. In contrast, Union Pacific (NYSE:UNP) can sometimes be viewed as a proxy for the broader US economy, given its exposure to commodities, agricultural products, chemicals, energy, and finished durable goods. Since mid to late 2022, economists and Wall Street have anticipated a recession in 2023 and 2024; however, the probability of a recession continues to fluctuate. At the end of March, Bloomberg reported that the odds of a US recession by March 2024 stood at 65%, up from 60% from the prior month. And with the Fed hiking rates by 25 bps at the May meeting to a 5.25% terminal rate, the probability of recession continues to inch higher. The looming debt ceiling expiration also presents a severe macroeconomic risk for all businesses.

While the general trend of economic softening intuitively bodes poorly for Union Pacific’s revenue growth over the coming quarters and years, there are still key areas where the trends are not as straightforward. For instance, US housing starts have remained resilient despite financing costs reaching levels not seen since the GFC. Additionally, the supply bottlenecks from the pandemic having almost entirely subsided have led to more significant overseas automobile shipments. These represent two areas that Union Pacific can leverage to outperform the forecasted decline in industrial activity in 2023. However, these niches will not be enough to overcome widespread economic stagnation.

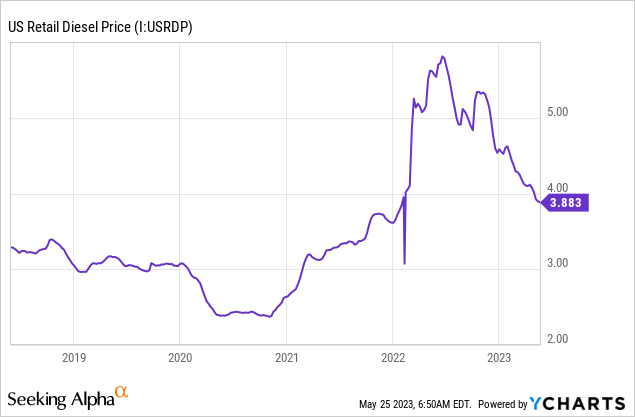

Apart from top-line trends, Union Pacific also continues to face high fuel costs that have hurt margins, but lower diesel prices compared to the highs of early 2022 should provide room for increased efficiency. The railroad operators continued adoption of PSR practices also poses a risk regarding long-term viability in the wake of major derailments which have captured public and Congressional attention. Thus, the conflicting elements at the macroeconomic and business-specific levels lead to my view of Union Pacific as a hold.

Top Line Remains a Mixed Bag

Union Pacific categorizes its freight into three main groups: bulk (including grain, fertilizer, coal, and food product), industrial (including chemicals, plastics, metals, minerals, forest products, and energy), and premium (automobiles and intermodal). Despite the growing warning signs regarding the broader economy, UP reported top-line gains in all three categories in their Q1 earnings, showcasing Y/Y growth for bulk, industrial, and premium of 4%, 3%, and 5%, respectively. Within these groups, the areas that experienced the most significant growth were automobiles (17% Y/Y), metals and minerals (11% Y/Y), and energy (11% Y/Y); the biggest declines were in intermodal (-3% Y/Y) and forest products (-9% Y/Y). Overall, the company experienced a decrease in volume for Q1 2023, offset by an increased fuel surcharge to combat inflationary pressures that have hit diesel fuel exceptionally hard.

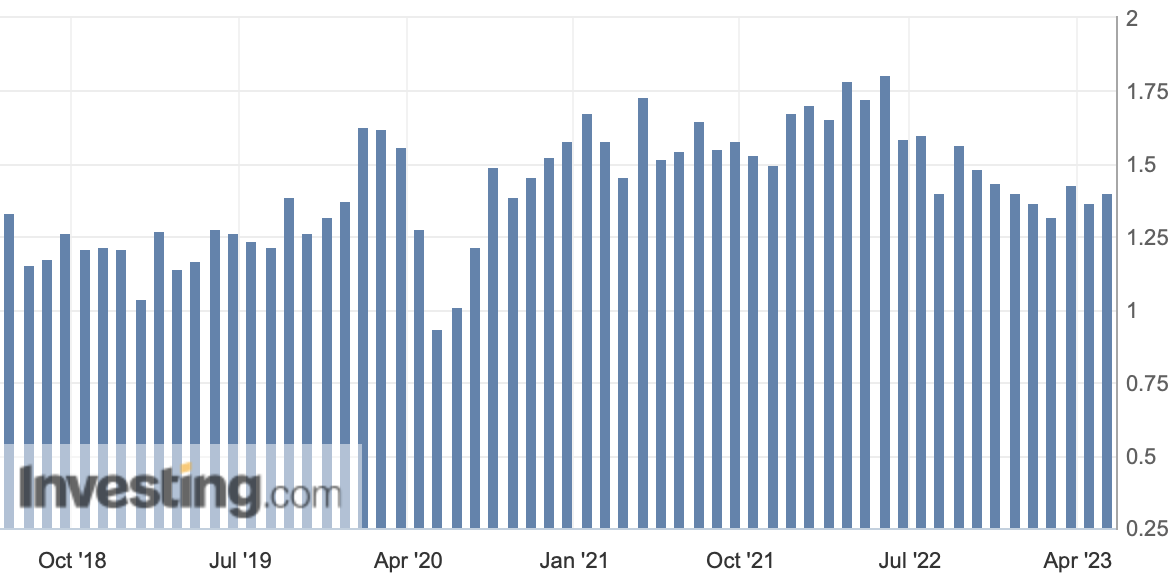

Looking forward, while many of UP’s end markets would pull back due to the recessionary environment, some select areas could continue to provide steady growth for UP. One area is forest products which a more resilient housing market could support. As of May 24, the fixed 30-year mortgage rates hit 7% again, according to Mortgage News Daily. Additionally, housing prices nationwide have experienced the largest Y/Y decline over a decade, falling 4.1% in April. Yet, despite these signs that signal a cooling in the housing market, housing statistics paint a different picture. For example, housing starts for April topped estimates at 1.401 million, still higher than pre-pandemic levels.

US Housing Starts; annualized change in residential buildings that began construction during given month. (Investing.com)

Additionally, homebuilders’ Q1 earnings suggest sustained demand in the housing sector. For instance, PulteGroup (PHM) reported lower cancelation rates, increased order backlog to over 13,000 homes ($7.9 billion), and a 6% Y/Y increase in closings. Other homebuilders reported similar trends, qualifying the assertion of a deteriorating housing market. I mention these trends because UP’s forest products find use in the housing end markets which also have the highest average revenue per car (APC). While UP reported sizable declines in Q1 in forest products from a softer housing market, limited housing supply due to homeowners being unwilling to sell in a high-rate environment and a cautiously optimistic outlook for homebuilders suggests UP could see upside potential in this freight type.

The automobile freight also presents a possible upside as car dealers continue to replenish depleted inventories that COVID and a semiconductor shortage stalled. Thus, ongoing recovery from COVID still provides a tailwind for some regions of UP’s business.

However, as stated previously, UP remains highly exposed to the US economy, and the consumer side will present a headwind for UP as consumers cut back on discretionary spending. As reported by CNBC, US consumer credit card debt stands at nearly $1 trillion, particularly concerning as the typical debt paydown following the holiday season did not occur as anticipated. In addition, as consumers continue to trim their purchases, retailers and consumer brands have faced considerable inventory bloat, notably large firms like Target (NYSE:TGT) and NIKE (NYSE:NKE). As an effect, these companies have cut back on orders for new inventory which has been reflected in UP recording a 3% Y/Y decline in intermodal “due to high inventories and inflationary pressures impacting consumer demand.” Other areas, like chemicals, will also face pressure due to a softening industrial landscape. As EVP Kenny Rocker stated in the earnings call, “Industrial chemicals and plastics volume was down 2% year-over-year driven by lower industrial chemical shipments due to challenged industrial production and reduced housing demand.”

The headwind that a sluggish economy presents outweighs the niche opportunities UP has to maintain revenue growth for 2023. Currently, consensus estimates for FY 2023 revenue stand just below FY 2022 revenue at $24.76B (Source: S&P CapIQ Pro). While I believe, as do many on Wall Street and in government, that the looming US debt ceiling fiasco will subside and a deal will be reached, growing uncertainty about US credit quality or the nightmare scenario of default would severely dampen the US economy and exacerbate projected revenue sluggishness for UP.

Controlling What Can Be Controlled

UP cannot control the direction of the US economy and thus cannot endow itself with revenue growth if everything pulls back; however, it can manage its internal operations and maximize profit from its stickier revenue streams. The market has already begun to price in the slowdown for the rails sector-wide from a softening economy: UP trades around 18x TTM earnings compared to 21.6x in December 2022, CSX (NASDAQ:CSX) trades near 15.7x compared to 18.5x, and Norfolk Southern (NYSE:NSC) trades around 16.3x versus 20x. Despite the unknown of the broader economy through the end of this year, UP’s catalyst for success over the near term lies in its ability to streamline operations and enhance efficiency.

One item that has weighed heavily on UP and all the railroad firms is oil prices. In the most recent earnings, management acknowledged that much of the Q1 revenue growth arose from higher fuel surcharges that mitigated the adverse effects of persistent energy inflation. Fuel costs have weighed UP’s margins since 2021 and continue to pressure the bottom line. In FY 2022, UP reported a 68% increase in fuel costs; for Q1 2023, the company reported a 7% Y/Y increase in energy costs. Luckily, diesel prices have steadily declined since late last year as supply and demand stabilized. While still elevated compared to pre-pandemic years, lower fuel costs will alleviate some pressure that drove UP’s operating ratio higher in Q1.

It would not be adequate to mention UP without discussing its continued integration of precision scheduled railroading (PSR) into its operations. I’m skeptical regarding the long-term viability of the practice and whether or not it will mainly prop up near-term profits at the expense of long-term success. Particularly in the wake of the Norfolk Southern incident in East Palestine this February, the growing movement among the Class I railways to adopt PSR for tighter operating ratios could do just the opposite if the PSR changes lead to another national headline derailment or a major labor dispute which Congress had to break late last year. The East Palestine derailment revamped calls for increased rail safety, with Republicans even backing regulations that would tighten rail safety standards. Ohio senators J.D. Vance and Sherrod Brown introduced the bipartisan Railway Safety Act to increase preventative measures, among other requirements such as mandating two-person crews. Not only would the bill introduce higher costs for railroads like UP, requiring additional labor costs and likely reducing the efficiency of the railroad to meet new safety standards, but it also epitomizes renewed public criticism of the railroads’ safety practices. And under PSR, the use of longer trains with less manpower further fits the narrative that the railroads seek to maximize profit at the expense of employee, environmental, and community safety, a perception that could hasten the timeframe for tighter regulations that dampen UP and other railway’s operating ratios. Therefore, the components of PSR, while aimed at reducing operating costs for UP, could be its undoing if the changes lead to another major derailment.

Additionally, the adoption of PSR has provided ambiguous results. When CEO Lance Fritz announced the adoption of PSR in 2018, he stated that PSR should deliver an operating ratio of 60% by 2020 and 55% over the longer term. However, for FY 2022, UP reported an operating ratio of 60.1% and 62.1% for Q1, a 2.7 percentage point increase from the prior year. And while fuel charges primarily attributed to the greater inefficiencies, UP has also seen greater inefficiency in terms of performance. Many opponents of PSR claim that the method often leads to longer customer delays. Since 2020, UP’s intermodal car trip plan compliance rate, which measures the percentage of cars delivered in line with scheduling, dwindled from 81% in 2020 to 67% in 2022. While the company cites crew shortages as the main driver of the poor results, fewer employees fit within the framework of PSR, suggesting that the crew shortages over the past two years offer a glimpse of a potential long-term headwind associated with PSR. While the theory behind PSR could certainly expand UP’s profitability, the labor issues of the past two years, plus the growing criticism over rail safety, exemplify the delicacy of PSR: its success requires seamless execution and can be foiled by sudden changes in economic conditions. For this reason, I remain skeptical about the long-term viability of PSR as a solution to reducing operating costs for UP and other rails, especially given that it has increased customer delays and risks attracting more significant safety concerns from regulators, employees, and the public.

Valuation Not Enticing Given Macro Backdrop

Compared to the other Class 1 railroads, UP trades near the top end of the valuation spectrum. UP trades around 16.9x forward earnings compared to 15.9x for CSX and 15.7x for Norfolk Southern (Source: S&P CapIQ). Additionally, UP trades expensive to the GFC; on average, it traded 14.5x forward earnings from 2008 to 2010. While the looming recession predicted by economists and the Street likely will not rise to GFC levels (ignoring current US debt ceiling issues), UP’s current valuation exceeds that for most of the early 2010s during the economic recovery.

On a dividend basis, UP’s current expected dividend for 2023 of $5.20 per share implies around a 6% long-run dividend growth expectation, well below the realized dividend growth over the last ten years of nearly 15%. Thus, while peer and historical analysis of how UP traded during and near economic downturns implies the stock price faces further downward pressure, the current price seems to undervalue UP’s consistent dividend growth. This indicates that the market’s primary concern is the near-term economic headwinds rather than the company’s sustained success. As one of the two companies in the western US railroad duopoly, UP will remain an integral part of the US economy and be around for a while. However, as a critical cornerstone in the US economy, UP also tends to move the economy, which continues to flash recessionary signs.

Therefore, I view Union Pacific as a hold, for the near-term headwinds will continue to weigh on the company’s long-term prospects. Nevertheless, UP maintains a superior return on capital relative to the other Class 1s and generated $4B in levered FCF last year, supporting continued dividend growth and share repurchases. One key caveat is that investors should continue to watch UP’s development and integration of PSR techniques and practices along with the political backdrop surrounding the railroad industry. UP management, rail unions, and industry experts continue to share widely varying opinions on PSR’s feasibility and how regulations might shift over the coming years should lawmakers and regulators determine whether companies like UP have compromised public and environmental safety to pursue profitability.